So with the start of the new tax year (2016/17), there comes a new Personal Savings Allowance. This means that you are allowed to earn a certain amount in savings interest without paying any tax on it.

The limits that are applicable for 2016/17 are:

- £1,000 in savings interest for those who are basic rate taxpayers

- £500 in savings interest for those who are higher rate taxpayers

So, due to this change, banks and building societies will no longer be deducting tax from your savings at the source. Instead, if you are liable to pay any tax on your savings due to them exceeding this amount, you will need to either pay the tax to HMRC via your self assessment tax return, or else they will collect it via your tax code.

Not only has the Personal Savings Allowance been introduced, but also those earning under £16,000 (including savings) may also be entitled to make use of all of part of the starting rate of 0% on £5,000 worth of savings interest.

For example, if you earn £9,000 in taxable income, then you can use the £5,000 savings interest allowance and the £1,000 personal savings allowance so you could effectively get £15,000 in tax free income.

Using the above example if you earned £11,000 in taxable income then the maximum you could earn and not pay tax is £17,000.

This obviously assumes that you have conveniently apportioned earnings from taxable income and savings but it is unlikely to be the case for the majority of people.

So if you earn more than £11,000 (the personal allowance for 2016/17) then you will only get some of the £5,000 starting rate if your earnings are below £16,000 – say you earn £13,000 then you can have £3,000 of the starting rate savings allowance.

But whatever you earn – as long as you pay basic rate tax or no tax at all – then you are allowed the £1,000 personal savings allowance.

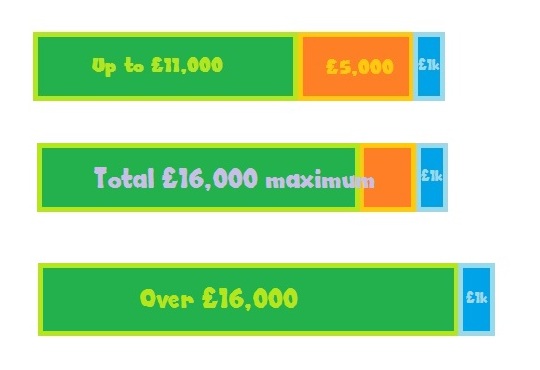

This graphic may help illustrate the effect for basic rate taxpayers of the personal Savings Allowance (up to £1,000 in interest from savings) and the starting rate savings allowance (up to £5,000 for lower earners)

In green are your taxable earnings, in orange is the available 0% rate on £5,000 worth of savings for lower earners and in blue is the new personal savings allowance of £1,000 for all lower rate taxpayers.

Any savings that fall out of these brackets are taxable.

For higher rate taxpayers you can have £500 in savings interest tax free and anything over that is taxable at your highest rate.